‘Tis the Season for Secure Payments: Protecting Your Business from Holiday Fraud

With shoppers feeling the pinch of inflation over the last year, the holiday spending outlook is a mix of cheer and bah, humbug. Just more than one-quarter (27%) of consumers plan to spend less this year than last, but slightly more (28%) plan to spend more, according to Boston Consulting Group research.

And a large portion of those consumers will be doing their holiday shopping online. In 2023, global online retail sales reached an estimated $5.8 trillion U.S. dollars globally, and projections show an expected 39% growth rate, with the global totals to exceed $8 trillion by 2027. And despite high inflation in 2024, holiday sales are expected to increase between 2.5% to 3.5% this year, bringing the total to between $979.5 billion and $989 billion, according to National Retail Federation information. E-commerce holiday sales will reach between $289 billion and $294 billion in 2024, according to research by Deloitte, compared to $252 billion in 2023.

While that’s overall good news for businesses, it also means competition for buyers’ attention (and cash) is fiercer than ever. To make sure your business stands out among other companies vying for consumers’ holiday purchases, focus on keeping your company and your customers safe from that ever-present Grinch: holiday fraud. Here are three ways you can keep your customers’ (and therefore your own) holiday merry and bright:

1. Hosted Payment Pages Are Your Digital Shield

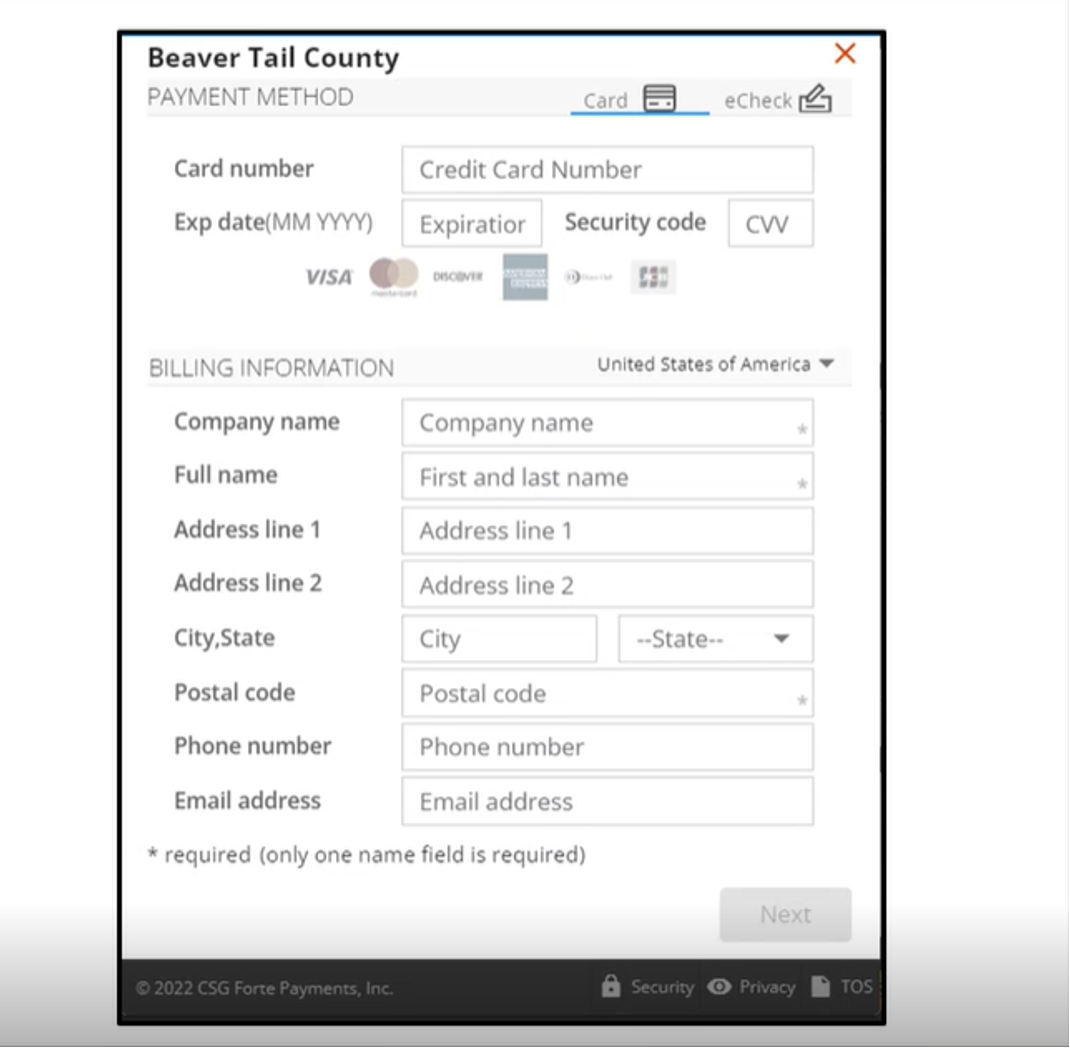

The global community continues to adopt online payments at breakneck speed—65% of adults reported using a digital wallet at least once a month. And all that money moving around means cybercriminals are eager to find ways in. That’s why safeguarding your customers’ payment data on securely hosted payment pages with a reliable payments provider should be top of your holiday to-do list. By directing your online payments through secure pages, you’re ensuring that sensitive payment data doesn’t linger in your system like a misplaced ornament.

What’s so special about securely hosted payment pages? Both your company and your customers are safe, and transactions are seamless. Customers enter their payment details on a page hosted by the payments provider, keeping the crucial data away from your servers and reducing your PCI (Payment Card Industry) Data Security Standard scope. This ensures a worry-free experience for both you and your customers that leaves would-be fraudsters out in the cold.

2. Digital Wallets: Secure, Convenient—and Gaining Popularity

There’s no better gift to offer your customers than secure and convenient digital payment methods. That’s why offering your customers payment options using their preferred digital wallet is guaranteed to put you on their “nice” lists. With enhanced security features, digital wallets provide a seamless, hassle-free and speedy checkout experience.

By offering popular digital wallets at your checkout, you’re not just embracing the holiday spirit—you’re also aligning with what consumers trust. Because digital wallets have such a robust safety record, consumers are trusting their services more and more. In fact, more than half (57%) of respondents to a National Retail Federation survey say they plan to use digital channels for their 2024 holiday purchases, and more than three-quarters (76%) of respondents to a Bain & Company survey said they planned to buy at least half of their holiday purchases online, creating more opportunities for bad actors’ schemes to steal valuable data. That’s because digital wallets safely store payment credentials and employ advanced encryption techniques to keep them protected. It’s a win-win—customers get a seamless payment experience, and you get the peace of mind that their data is protected.

3. Use Tokenization to Thwart Fraudsters

While fraudsters will always try and bring a little Grinch to the holidays, you can keep them off your payments platform (and on the “naughty” list) by replacing actual card and ACH payment data with generated randomized tokens. This “tokenization” converts your customers’ sensitive personal information into tokens that have no intrinsic value and provide no value to fraudsters—you can think of it as the equivalent of leaving fake presents under the tree for anyone attempting to snatch them. A reputable payments provider can assist you in implementing this robust layer of security, ensuring that even if a Grinch manages to sneak into your system, they leave empty-handed.

Don’t let the fear of fraud steal your joy this holiday season. By following these three tips—utilizing hosted payment pages, offering secure digital payment methods and embracing tokenization—you can ensure your online business stays secure while shoppers stuff their carts.

CSG Forte is here to protect your payments this holiday season. Contact us to get started today.