What Do ACH Credits Mean & How Do They Work?

Do you compensate your employees through direct deposit? Have you paid your bills online? If so, you have sent ACH credit. The Automated Clearing House (ACH) is a critical network in the United States financial industry that manages millions of transactions like these every day.

ACH credit makes electronic money transfers possible, so many systems and apps use this infrastructure for digital payments. You can benefit from fast, simple and secure payments when your business uses ACH payment solutions.

Read our guide to understand the meaning of an ACH credit and how it can boost your business.

What Is ACH Credit and What Does It Mean?

An ACH credit is an electronic payment that sends money from one account to another. The payer (the person sending the payment) makes the request to push funds from the originating bank account (the payer’s account) to the recipient (the person receiving the payment) by putting the funds in the deposit account (the recipient’s account).

This method requires only a few basic transaction details, including the payer’s and recipient’s:

- Name

- Bank account number

- Bank routing number

In just a few hours or days, the transaction is completed, and the recipient has the funds in their account.

ACH credits occur through ACH, an electronic money network connecting every major financial institution in the country, including credit unions, banks and the Federal Reserve. With this network, people and businesses can facilitate payments between accounts regardless of the banking institution. The National Automated Clearing House Association (Nacha) manages the ACH network and ensures payment is safely and quickly transferred. While this network mainly transfers money within the U.S., it can be used for international transfers.

How Does ACH Credit Work?

ACH credits are essentially a digital form of paper checks. With a paper check, the payer would fill out a check for the recipient to take to their bank. With credit ACH, the details are recorded and the funds are transferred electronically.

Here is how ACH electronic credits work:

- The payer initiates the payment: The payer provides the originating bank—or the Originating Depository Financial Institution (ODFI)—with the recipient’s account number and routing number, the amount of money to transfer, and a target settlement date (the date to transfer the money).

- The ODFI sends the payment details to ACH: The ODFI or their approved processing partner starts the transfer by sending the request to the ACH network. These institutions may batch several transactions to send to ACH in bulk.

- ACH sends the details to the recipient’s bank: The ACH network receives incoming transfer details in bulk and breaks them down into individual transactions. They bundle the transactions into batches and send the batch to the depositing bank—or the Receiving Depository Financial Institution (RDFI). ACH completes this process five times per business day.

- The RDFI processes the transaction: The RDFI receives the ACH bundles in their system and executes the transaction based on the processing window. Any transactions with incorrect information will trigger an error code, and the RDFI sends error codes back to ACH.

- The ODFI and RDFI settle the transaction: If the transaction has the correct details, the ODFI and RDFI settle the payment using their Federal Reserve balances.

- The recipient receives the payment: The RDFI releases the ODFI funds to the deposit bank account.

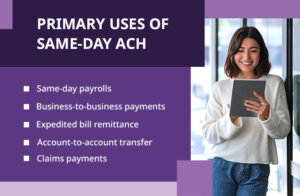

This process typically takes two business days, but it can be completed in one day if the ODFI pays a fee for same-day processing.

Examples of ACH Credit

Many individuals and businesses use ACH credit every day without realizing it. Any payment involving an account number and routing number to transfer money counts as an ACH transfer.

The most common examples of ACH credits include:

- Online purchases: For merchants that do not accept credit card payments online, consumers can use an ACH transfer to pay the store for their order.

- Refunded purchases: When merchants need to refund a consumer for a returned product, they can push money from their account to the consumer’s account. This transaction is an ACH credit.

- Government benefits: The U.S. government uses ACH credit to send money from its accounts to qualified recipients for stimulus payments and similar transactions.

- Direct deposit: When employers send payroll to employees through direct deposits, these transfers are a type of ACH credit. Funds in the employer’s account are pushed to their employees’ bank accounts.

- Bill payments: Many companies allow customers to pay their bill online. Customers can provide their account and routing numbers to transfer funds from their account to the business to settle the bill.

- Peer-to-peer payments: Payment apps like Venmo and PayPal allow people to send money to another person. This transaction is an ACH credit payment.

ACH Credit Fees

While an ACH credit transaction is free, fees may be incurred depending on the bank used. If the ODFI or RDFI uses a processing partner, the partner may charge additional fees. The bank itself may charge a fee per transaction. The fee for an ACH credit transaction can range from tens of cents to a couple dollars.

Factors that impact ACH credit fees include:

- The number of transactions processed per month

- The monetary amount of transactions

- The likelihood the transaction will be returned

- If the transaction requires same-day processing

- Which account validation method will be used

Since these fees operate on a scale, businesses will see reduced costs per transaction the more transactions they have.

What Are The Benefits of ACH Credits For Your Business?

Compared to traditional payment methods, ACH processing is quicker, easier and more secure. ACH transactions offer many advantages, including:

- Simple setup: ACH credit requires the payer’s and recipient’s bank account number and routing number. By requiring only a few details, your business can easily set up one-time or recurring payments. Because these numbers change infrequently, if ever, you can count on your payments to go through.

- Minimal to no transaction fees: Compared to wire transfers and credit cards, ACH credit fees are much lower, if there is a fee at all. This cost-effective fee pricing leads to monetary savings for your company.

- Fast payments: ACH credit is one of the most efficient payment methods available. You can pay your employees and bills right away without manual processing. Funds move quickly between banks and are available in the deposit account as soon as the transaction is finalized.

- Enhanced security: Credit ACH transactions have many security measures to ensure the funds are safe between the originating and deposit accounts. For example, bank account verification requires the payer and recipient to prove their bank account numbers, and fraud detection verifies the parties’ identities.

- Accessible payment records: You can review electronic records of your transactions in your ACH processing platform at any time.

Choose CSG Forte for ACH Payment Solutions

Your company can process ACH payments from any device, bank or source with validate services from CSG Forte. We offer two solutions—Validate and Validate+—to process and report your payments while reducing manual errors and identifying bad checks before processing. Your business can also validate online transactions for fraud, keeping you compliant with Nacha.

Contact us for more information about Validate and Validate+ or sign up today for your payment processing solution.